Add your promotional text...

Analysis Report: The Escalating U.S.–China Trade War and Its Global Implications

This report analyzes the intensifying trade conflict between the U.S. and China, exploring its causes, developments, and impact on global markets. It highlights the far-reaching economic and geopolitical consequences of the ongoing trade tensions.

4/10/20254 min read

Executive Summary

The United States has launched a dramatic escalation in its trade war with China, imposing punitive tariffs of over 100% on Chinese imports. In retaliation, China has raised its tariffs on American goods from 34% to 84% and warned that it will “fight to the end” rather than yield to what it labels U.S. coercion. This tit-for-tat escalation is not merely bilateral—it puts over $585 billion in annual trade at risk and poses a significant threat to global economic stability.

The fallout from this confrontation is already evident: inflationary shocks, collapsing investor confidence, disrupted supply chains, and the specter of a global economic slowdown. What began as a strategic trade dispute has morphed into a systemic crisis, with broad implications for consumers, producers, financial markets, and global institutions.

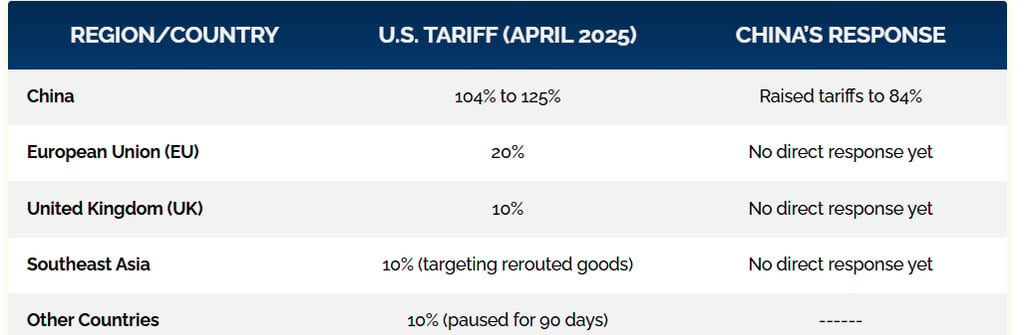

I. Escalation Timeline: A Breakdown of the April 2025 Tariffs

Source: BBC News (2025), New York Post (2025), News.com.au (2025)

II. U.S.–China Trade Dynamics: Pre-Escalation Snapshot

• U.S. Imports from China (2024): $440 billion

• China’s Imports from the U.S.: $145 billion

• Resulting Trade Deficit: ~$295 billion (≈1% of U.S. GDP)

Top U.S. Imports from China:

• Smartphones (9% of all U.S. imports from China)

• Electronics, toys, EV batteries

• Many sourced through U.S. multinationals like Apple

Top Chinese Imports from the U.S.:

• Soybeans (to feed 440 million pigs)

• Petroleum, pharmaceuticals

III. Domestic Consequences in the U.S.: A Manufactured Economic Crisis

A . A Fragile U.S. Economy, Even Before the Tariffs

Consumer sentiment was deteriorating prior to the escalation. Inflation expectations reached 5% year-over-year, while actual inflation hovered closer to 2%. Consumer confidence hit a 12-year low, with rising auto repossessions and falling housing affordability (Dayen, 2025). Commercial vacancy rates peaked at 20% nationwide.

Manufacturing—a key target of protectionist rhetoric—was already shrinking, with new orders falling and factory jobs disappearing. Durable goods prices were rising due to earlier trade tensions and global material shortages.

B. Tariff Shock Erratic Policy Amplies Downturn

The April 2025 tariffs functioned as a blunt economic instrument. Rather than strategic, targeted protection, the White House imposed sweeping hikes across all Chinese imports. The result: soaring input costs, higher prices for consumers, falling stock prices (Apple lost 20% of its market value), and worsening inationary pressures.

C. Stagation and Financial Contagion:

The U.S. faces rising ination without economic growth—classic stagation. Lending markets are tightening, with AI-driven risk models denying business loans. Forecasters like Yardeni Research have raised recession probabilities to 45%, while the UCLA Anderson Forecast warns the economy is “on recession watch” (Dayen, 2025).

There is growing concern that nancial contagion could spill into the bond market. As economist Adam Tooze notes, a forced selloff of U.S. Treasurys by leveraged investors could send yields soaring and damage global condence in the dollar as the world’s reserve currency.

IV. China’s Countermeasures and Strategic Response

A. Tariff Retaliation and Export Leverage

China’s retaliatory tariffs target key U.S. exports—particularly soybeans, petroleum, and pharmaceuticals. But Beijing may escalate further by restricting exports of critical industrial inputs such as gallium and germanium—metals vital to defense, semiconductors, and AI development.

B. Supply Chain Rerouting and Evasion

To counter previous tariffs, Chinese rms increasingly routed goods through Southeast Asia— Vietnam, Malaysia, and Thailand. The U.S. has responded by extending tariffs to these re-export hubs (BBC, 2025), sparking broader regional disruption and signaling an intent to close all loopholes.

C. Diplomatic Counterpressure

Beijing may seek alliances through alternative trade routes and organizations (e.g., BRICS+, RCEP). It may also pressure third countries economically to resist U.S. demands for trade alignment, accelerating the global trend toward economic blocs.

V. Global Economic Impacts: Beyond Bilateral Tensions

1. Global Supply Chains Disrupted

The new tariffs and retaliations are already destabilizing just-in-time supply systems. Electronics, auto parts, and clean energy components are delayed, leading to higher global production costs and delivery times.

2. Inationary Pressures Worldwide

The U.S. tariffs on core consumer goods—smartphones, batteries, toys—are likely to push prices upward globally. U.S. ination could spike past 4% annually, dragging global ination along due to the dollar’s centrality in trade.

3. Rare Earths and Strategic Materials

China’s control over 70% of global rare earth processing capacity gives it enormous retaliatory leverage. Restrictions could impact military contractors, EV manufacturers, and chipmakers across Europe and Asia.

4. Risks to Global Growth and Stability

With the U.S. and China comprising 43% of global GDP (IMF, 2025), any synchronized downturn could trigger a worldwide recession. Countries dependent on global trade are bracing for reduced capital ows and rising import costs.

5. Steel Dumping and Market Oversupply

China’s nearly $1 trillion export surplus (BBC, 2025) may now target new markets with subsidized goods—especially steel and aluminum. The UK steel industry has already raised alarms about unfair competition from Chinese oversupply.

VI. Strategic and Political Dimensions

• Economic Nationalism:

The U.S. is increasingly using trade policy to secure geopolitical inuence, signaling it will penalize nations (e.g., Mexico, Cambodia) that fail to align against China.

• Decoupling Trend:

The conict has evolved beyond tariffs—now incorporating tech access, materials control, and third-country coercion.

• Multilateral Institutions Undermined:

The World Trade Organization has been sidelined, and the rules-based global order is fraying under unilateral moves from both sides.

VII. Outlook: Strategic Scenarios and Policy Options

VIII. Conclusion

The April 2025 escalation in U.S.–China tariffs marks a historic turning point in global trade relations. What began as a dispute over trade imbalances has metastasized into a full-scale economic conflict with global reach. Inflation is rising, production costs are surging, and systemic risks to the dollar and global financial stability are now material.

This is not an inevitable crisis—it is a policy-induced one. De-escalation, multilateral engagement, and a recalibration of global trade priorities are urgently needed. The longer both powers pursue decoupling through coercive economic tools, the greater the long-term harm to their own citizens— and to the world economy.

Stay informed with our latest project news.

Connect

info@strategiccentre.org

© 2025. All rights reserved.

media@strategiccentre.org

Terms & Policy

Stay UPDATED